Did you know Home First Finance grew over 35% CAGR and disrupted India’s housing finance market by focusing on chaiwalas and kirana shop owners who banks ignore? Here’s a deep dive into how they did it—and why MBA freshers love (and sometimes leave) HFFC

Let’s go through this news

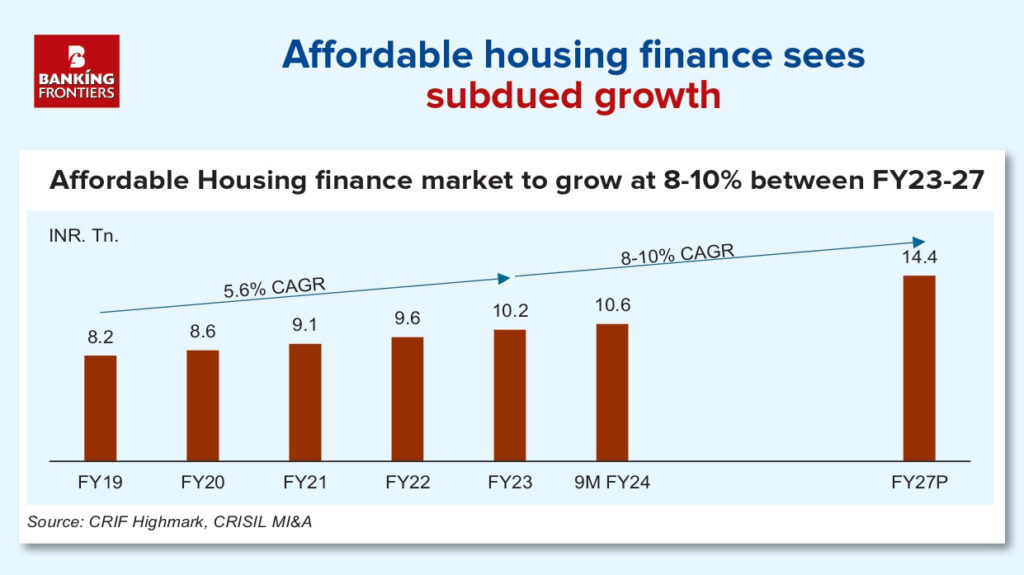

affordable housing finance company going to almost 15% CAGR growth in next 2 years , projection 77-81 lakh crore in 2030.

top affordable housing finance list 2023

(In Below link home first is on 8 rank )

Despite facing intense competition from both government-backed and private housing finance home first result market mojocompanies, Home First Finance Company stands out due to its speed, service, flexibility, and customer-centric approach.

In October 2020, Warburg Pincus acquired a 25% stake in Home First Finance for ₹700 crore.[15] In January 2021, Warburg Pincus increased its stake to 30.62% ahead of Home First Finance’s initial public offering.

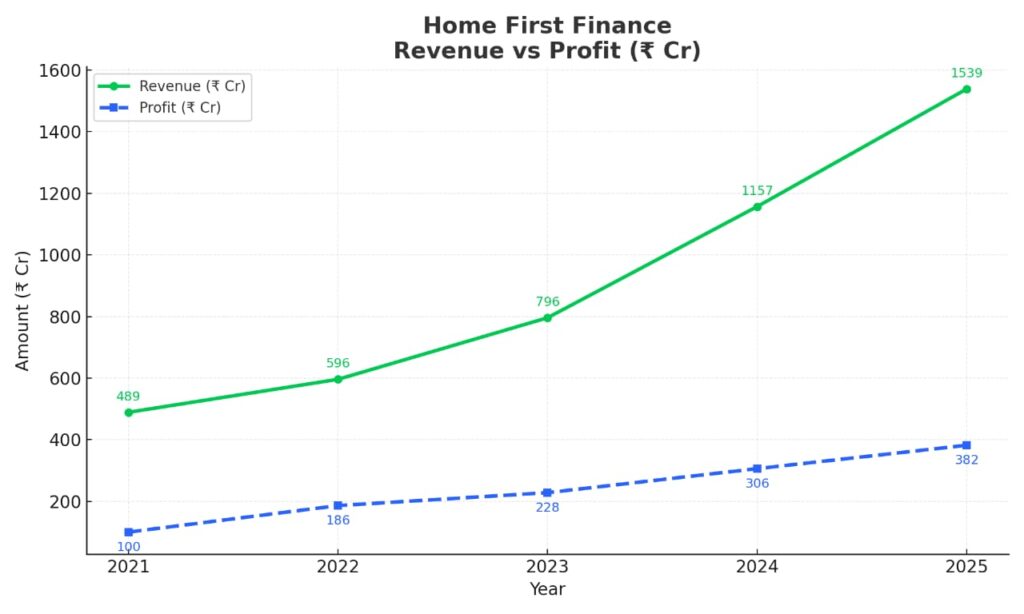

With an impressive CAGR of over 35% in the last 5 years, Home First Finance has built a sustainable and scalable business model, currently operating with 150+ branches across India and serving 1.5 million+ happy customers .

Founded in 2010 by Manoj Viswanathan (Ex-Citigroup India) and P.S. Jayakumar (former MD & CEO of Bank of Baroda), Jerry RaoHome First Finance was born out of a deep understanding of the gaps in the Indian housing finance market. Traditional institutions often fail to serve informal sector customers like Kirana store owners, Vadapav vendors, Chaiwalas, and vegetable sellers.https://www.marketsmojo.com/stocks-analysis/total-returns/home-first-finan-1003457-0

With a mission to bridge this gap, Home First Finance focuses on providing fast, flexible, and accessible home loans to middle-class and lower-middle-class customers, particularly in Tier 1, Tier 2, and Tier 3 cities.🔗 Home First Finance Company India Ltd

Their commitment to empowering informal sector families with home ownership has made Home First Finance a leader in affordable housing finance in India.

🔗 : Home First Finance Company

Problem with the Govt and Top private Banks : Banks like SBI ,HDFC ,UNION , they cannot have customer Centric Apporoch , and the main point where home first comes into play is that govt bank don’t give home loans to informal customer who don t have salary slip or No ITR .

Top Features That Make Home First Finance a Leader in Affordable Housing Loans.

- ✅ 48-Hour Loan Sanction – Fast approval process to save your time.

- 💻 100% Digital Process – From application to disbursal, everything is paperless and hassle-free.

- 🤝 Dedicated Relationship Manager – One-on-one support for every customer throughout the loan journey.

- 👨👩👧👦 Family Income Considered – Loan eligibility is calculated based on total household income.

- 💸 Zero Charges for Part-Payment or Loan Transfer – Flexibility without hidden costs.

- 📄 No Salary Slip or ITR? No Problem! – Home loans available even without formal income proof.

- 📊 CIBIL Score of 650+ Accepted – Loans available for customers with moderate credit scores.

- 🚀 Loan Disbursal Within 7 Days – Quick and efficient disbursal process.

- 🪪 Simplified KYC Process – Easy documentation to speed up your application.

- 💼 Strong Financial Backing – Supported by reputed investors and institutions.

- 🌟 High Customer Satisfaction – Trusted by over 1.5 million happy customers across India.

http://Home First Finance Company India’s net profit up 23.55% in Q3 FY25 – ET Realty

Home First Finance is committed to empowering lower and middle-class families in India by providing accessible and affordable home loans, especially in Tier 1, Tier 2, and Tier 3 cities. The company focuses on bridging the gap in housing finance by offering a completely digital, fast, and flexible loan process tailored to the needs of underserved communities. With interest rates ranging between 8% and 14%, depending on key factors like credit score, income level, age, and repayment capacity, Home First Finance ensures that customers receive customized financial solutions without the burden of excessive documentation or delays. Their mission is rooted in the belief that every family deserves a home, and through innovative technology and dedicated service, they make homeownership possible for those who traditionally lack access to formal credit. By simplifying the loan journey and offering personalized support, Home First Finance stands out as a trusted partner for families aspiring to own a home in India’s growing urban and semi-urban areas.

- Home loan

- LAP

- RESELL Properties

- Construction purpose

- Shop loans

Home loans helps people to buy new or old house, and they pay it back every month in small parts called EMIs. If someone already have a property like house or shop, they can take Loan Against Property (LAP) by keeping that property as security and use money for things like business or education. Resale property loan is for buying old house from someone else, and it need more paper checking. Construction loan is given to those who have land and wants to build a house on it, money is given step by step as work goes on. Shop loan is taken by people who wants to buy or build shops or offices for business purpose. These all loans help people to buy, build or use property in better way.

Why HFFC’s Customer Verification Model Stands Out

One of the biggest differences between Home First Finance (HFFC) and other Housing Finance Companies (HFCs) working in the affordable housing sector—like Aavas, HDFC, SBI, Piramal, or Aditya Birla Housing Finance—is the way customer verification is handled.

Most traditional banks and big HFCs rely on third-party verification agencies to collect and validate customer details. These external agencies often visit the borrower’s home or shop and submit reports to the lender. However, this process comes with challenges. The agencies have no personal connection with the customer and assess them purely based on what they observe at the moment—often missing the full picture.

Let’s take a simple example:

A chaiwala (tea seller) usually sells 50 cups a day, but if the verification agency visits him on a rainy day, he might only sell 40 cups. The agency notes this as low income and reports it to the lender—leading to loan rejection. There’s no flexibility, understanding, or relationship in this process. This often discourages genuine borrowers with informal income who don’t have fixed daily earnings.

On the other hand, HFFC follows a completely different approach.

They assign a dedicated Relationship Manager (RM) for every loan case. This RM takes care of everything — from sanction to verification, KYC, disbursal, and even collection. The RM builds a personal relationship with the customer, understands their real income pattern, and offers support and flexibility based on the borrower’s true potential, not just one-day observation.

This human approach creates trust, improves customer experience, and most importantly, speeds up the entire loan process. The loan gets disbursed faster, with fewer delays and misunderstandings. For lower and middle-income families, especially in Tier 2 and Tier 3 cities, this level of service makes a huge difference.

Home First Finance Company (HFFC) is well-known for its strong campus hiring across Tier 2 MBA colleges. Nearly 70–80% of its workforce is made up of MBA graduates from these institutions, making it a top choice for freshers entering the housing finance sector. With its focus on affordability and growth, HFFC has built a reputation as a company that gives opportunity to learn, earn, and grow quickly.

💼 Attractive Pay for Freshers

https://www.linkedin.com/company/home-first-finance-company?originalSubdomain=in

As of now, HFFC offers a starting package of ₹6 LPA to MBA freshers, which is well above the national average CTC offered by most HFCs and banks. In addition to full-time roles, HFFC also provides internships of 2–3 months, primarily in Business Development, giving students valuable real-world experience even before they graduate.

📈 Career Growth & Hierarchy

https://homefirstindia.com/careers?srsltid=AfmBOopa1e_crQMrYaHti0skVArUnW_Nkns2BxPgxZaOXLcPOXtOR2pZ

HFFC offers a clear and fast-paced promotion structure, especially for those in the field sales teams. The growth ladder includes:

- Relationship Manager

- Senior Relationship Manager

- Team Lead

- Branch Manager

- Cluster Manager

- Regional Sales Manager

Alongside sales, the company also has non-field roles like Credit Manager and Customer Service Manager, which are more branch-based and involve no field visits.

Full Finance Exposure from Day One

Unlike many other HFCs, at HFFC, a Relationship Manager handles multiple key departments—not just sales. They are involved in:

- Business Development

- Customer Verification

- Sanctioning the Loan File

- Credit Assessment

- Disbursal

- Collections

This gives freshers complete exposure to the loan lifecycle, making them job-ready in multiple functions of finance early in their career. For some, this feels overwhelming—but for many, it becomes a career accelerator.

Incentives and Promotions

HFFC rewards performance handsomely. Top performers can earn:

- Up to ₹15,000 in quarterly incentives for achieving targets

- Appraisals up to 30%, which is significantly better than industry standards

This fast-track growth system makes HFFC stand out for those who are ambitious and goal-driven.

Work Pressure Is Real

However, the journey is not without its challenges. HFFC roles involve:

- 95% field visits – long hours, travel, and customer follow-ups

- High pressure at month-end, which means less chance of leave or holidays

- Daily target chasing and multitasking across departments

According to AmbitionBox reviews, around 95% of freshers leave HFFC within the first year, mainly due to the field workload and pressure.

https://homefirstindia.com/blog/

- “Home First Finance: A CredITable trailblazer – the FIRST among equals” (PDF). Motilal Oswal. Retrieved 28 September 2022.

- ^ Jump up to:a b c d “Annual Report 2023-24” (PDF). Home First Finance Company India Ltd. Retrieved 8 June 2023.

- ^ “Home First Investor Presentation Q4 FY24” (PDF). Home First Finance Company India Ltd. Retrieved 8 August 2024.

- ^ “Home First Finance Company India Limited”. ICRA. Retrieved 8 June 2023.

- ^ “Home First Finance Company India Ltd” (PDF). Edelweiss Research. Retrieved 27 September 2022.

- ^ “Home First Finance” (PDF). ICICIdirect. Retrieved 27 September 2022.

- ^ Jump up to:a b “Home First Finance debuts at 19% premium over issue price”. The Economic Times. Retrieved 27 September 2022.

- ^ Nandy, Madhurima (1 February 2013). “Jaithirth Rao | The late homebody”. mint. Retrieved 27 September 2022.

- ^ “Warburg ‘looking to exit’ from Home First Finance”. Business Line. The Hindu. Retrieved 28 September 2022.

- ^ “National Housing Bank – Annual Report 2010-2011” (PDF). nhb.org.in. Retrieved 27 September 2022.

- ^ Nandy, Madhurima; Unnikrishnan, Dinesh (9 June 2011). “US-based Bessemer buys stake in affordable housing finance start-up”. mint. Retrieved 27 September 2022.

- ^ Jump up to:a b “True North to invest $100 mn in Home First Finance”. VCCircle. Retrieved 27 September 2022.

- 104 immigrants'

- 1bhk

- affordable housing

- america

- b2b

- blog

- blogging

- broker

- chava

- dhayri

- digitalmarketing

- disbursement

- farmers

- finance

- flats

- hffc

- homefirstfinance

- homeloan

- indiamart

- jerryrao

- karvenagar

- katraj

- lap

- leadership

- linkdinblog

- loan

- management

- marathi

- marketing

- mba

- mbafresher

- mbastudent

- money

- nbfc

- nevillewadia

- pune

- puneflats

- realeste

- sambhaji

- students

- trending

- US

- uttekar

- vickykaushal